Energy demand is growing in India, but current renewable additions are not enough to meet this rising demand, let alone replace existing coal.

—

In Gujarat’s white desert, the Khavda renewable power plant is set to become the world’s largest clean energy installation, generating a staggering 30 GW of solar and wind power by 2030. Yet, across the country, a 3 GW coal-fired plant in Chandrapur, Maharashtra, continues to spew smoke, one among hundreds that still power over 60% of India’s grid.

This juxtaposition captures the central tension in India’s energy transition: How can a developing nation reconcile its growing hunger for energy with its increasingly ambitious climate goals?

Development vs. Decarbonization

Unlike developed economies, India is still growing. Its people still consume far less energy than the global average. Electricity provision – a given in the developed world – is still a development imperative here.

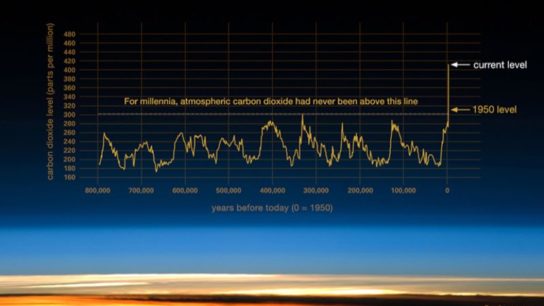

Over the past two decades, India has made remarkable progress in electrification. Thanks to targeted government programs, electricity access rose from just 60% in 2000 to near-universal coverage today, and electricity shortfalls have fallen below 1%. However, this electrification has been driven primarily by coal.

Coal capacity surged in the previous decades, and continues to rise, albeit more slowly. Today, the electricity sector accounts for over half of India’s emissions. While its per capita emissions remain low, India is now the world’s third-largest emitter of greenhouse gases.

Even so, India has emerged as a climate leader. Its 2015 Nationally Determined Contribution (NDC) pledged that 40% of its electricity capacity would come from non-fossil sources by 2030. In 2022, it raised that target to 50% and set a net-zero goal for 2070. Since 2015, India’s renewable capacity has grown nearly 20% annually, crossing 200 GW in 2024.

Still, as the world’s “well below 2C” window closes fast, attention is turning to India. While global emissions are expected to peak soon, India’s are still climbing. The country is projected to drive over a quarter of global energy demand growth through 2040. As the world is trying to phase out coal, why isn’t India able to move away from it?

Renewables Are Cheaper, But that Is Not Enough

Over the past decade, the costs of solar and wind have plummeted. On a levelized cost of energy (LCOE) basis – the average unit cost of electricity over a plant’s lifespan – renewables are now cheaper than coal. Even by variable cost comparisons, solar now beats coal. Then why are new coal plants still being built and planned?

The answer lies in what cost metrics do not capture.

A Kilowatt Isn’t Always a Kilowatt

Solar and wind – classified as variable renewable energy (VRE) – generate power only when the sun shines or the wind blows. A solar plant generates only 15-25% of its maximum output over a year – known as the Capacity Utilization Factor (CUF) – while wind averages 25-35%. A coal plant, in contrast, can run 24/7, with CUFs as between 70-90%. This means that much more VRE capacity must be built to meet the same demand, requiring greater upfront investments, especially challenging in a country where capital is expensive.

But the challenge isn’t just how much power is generated. It’s also about when and where.

Integration Challenges: Time and Space

A key challenge is timing. India’s power demand peaks twice daily: once at noon and again after sunset. Solar power helps with the former, but not the latter. And with solar making up the bulk of new renewable additions in India, there is little clean energy available after sunset, just when people return home and air conditioner use spikes.

This temporal mismatch between demand and supply could be solved through battery storage. Solar output during the day could be stored and used for nighttime demand. But utility-scale battery storage remains far from commercially viable. Another option is to use flexible fuels like natural gas: its generation can be ramped up or down quickly to complement renewable generation. Countries in the Global North rely on it to complement VRE. India, however, lacks the infrastructure for gas at scale. Instead, it relies on coal.

Coal is less nimble, and costly to turn on and off. As a result, coal plants are often kept running all day, even when renewable generation is high. This lowers their CUFs, and drives up their per-unit costs, since fixed costs are spread over fewer units of output. Paradoxically, it was the overcapacity of coal built in the previous decade that provided much needed flexibility to integrate VRE at scale. But it also drove coal CUFs to record lows.

Geography is another challenge.

While coal thermal plants can be built close to demand centres, India’s solar and wind resources lie far away. The Khavda facility, for instance, lies far from Gujarat’s industrial and urban hubs. Connecting these new energy sources requires massive new transmission infrastructure.

Moreover, India’s renewable potential and current installed capacity are geographically concentrated in six southern and western states. Meanwhile, coal-rich states in central and eastern India account for much less. And although India has a nationally integrated grid, actual dispatch and balancing are often done at the state level. So excess solar in Rajasthan cannot easily serve daytime peaks in neighboring states.

While transmission infrastructure is being expanded, it is struggling to keep pace with renewable deployment. This mismatch has led to curtailment – clean power that goes unused because the grid cannot absorb it – which has increased in multiple states in recent years.

These integration challenges – temporal, geographic and institutional – add hidden costs. They lower CUFs and increase curtailment, neither of which are captured in LCOE calculations. They also limit the share of VRE that can be integrated to the grid, regardless of how cheap it becomes. The remaining demand must be met by other sources, which in India’s case, is predominantly coal.

When Might Coal Peak?

Rahul Tongia, Senior Fellow at think tank Centre for Social and Economic Progress (CSEP), offers a useful framework: the Ladder of Competitiveness.

- Stage 1: VRE is costlier than new coal → Coal dominates new capacity.

- Stage 2: VRE becomes cheaper than new coal → Renewables meet some new demand, but coal persists. India is here today.

- Stage 3: VRE + storage becomes cheaper than new coal → Renewables meet nearly all new demand, coal additions stop.

- Stage 4: VRE + storage is cheaper than existing coal → Renewables start to meet demand earlier met by coal. Coal starts to decline.

A number of studies project India’s annual electricity demand growth at 6-6.4% until 2030. According to CSEP, meeting this demand without accounting for storage would require adding 46 GW of solar and wind each year, consistent with India’s 500 GW target. But factoring in storage pushes the number higher.

CEEW finds that once transmission constraints are included, the 500 GW target may fall short, but diversifying VRE capacity across states could help reduce the shortfall. Ember and TERI find battery costs keep falling by roughly 7%, India may remain in Stage 2 at least until 2032, when storage at scale becomes viable. Until then, VRE could meet over 75% of solar-hour demand, but only a third in non-solar hours, the rest met by coal.

Yet, actual deployment is lagging. Annual additions may be lower–20-30 GW for solar and 4-8 GW for wind. If that gap persists, coal dependency may grow further.

The Way Forward

Until storage scales, increasing the flexibility of India’s power system is key. Demand response measures such as Time-of-day (ToD) pricing could incentivize customers to shift demand to times when the supply is more plentiful, reducing the need for battery storage.

Grid operators need better real-time monitoring and control systems to manage intermittency, such as a sudden cloud cover over solar fields. Coal plant flexibility increases, such as ramping down during solar peaks and ramping up during time hours, could enhance supply flexibility, but doing so could be costly, making operators reluctant. Finally, transmission reforms, such as improving inter-state coordination could drastically reduce curtailment, cut emissions and minimise unnecessary coal additions.

Final Thoughts

We began with a striking image: the gleaming Khavda solar park and the aging Chandrapur coal plant. But perhaps framing India’s energy story as a battle is misleading.

India’s energy demand is still growing. Current renewable additions aren’t enough to meet this rising demand, let alone replace existing coal. So for now, it is coexistence – with coal filling gaps that renewables can’t yet close.

The stakes are global. How India balances its growth and decarbonization over the next decade will play a major role in determining whether the world can limit warming below 2C. But for now, the world may have to accept the fact that coal isn’t going anywhere anytime soon.

This story is funded by readers like you

Our non-profit newsroom provides climate coverage free of charge and advertising. Your one-off or monthly donations play a crucial role in supporting our operations, expanding our reach, and maintaining our editorial independence.

About EO | Mission Statement | Impact & Reach | Write for us

![The Statistics of Biodiversity Loss [2020 WWF Report]](https://earth.org/wp-content/uploads/2020/12/lprwinkyTHB-544x306.jpg)